Kleros - Compliance for the World Of Decentralized Finance

How does the current DeFi market compare to the 'coffee house regulation' of the 18th Century and what does it have to do with Kleros? In short - compliance.

How Kleros can secure the DeFi ecosystem...

A notable moment in world economic history was the creation of the joint stock company. It started in Amsterdam with the foundation of the Dutch East India Company and then in England.

By the end of the 17th century, shares of at least 150 corporations were traded at London's Royal Exchange, a market that also housed other merchants such as grocers, druggists and clothiers.

But the government looked down on the nascent stock market and, in 1696, passed an act to restrain the practice of brokers.

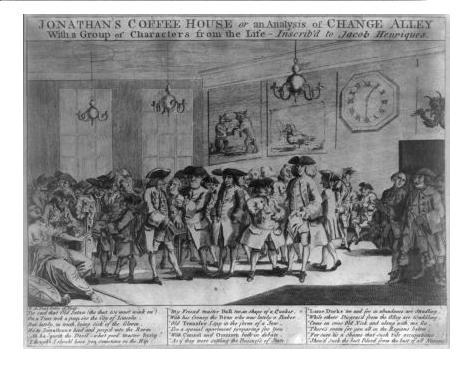

Expelled from the Royal Exchange, brokers congregated in Change Alley between Cornhill and Lombard streets in the City of London. In 1700, when the city government prohibited them from meeting on the street, their main trading venue became Jonathan’s Coffee House.

A market flourished where traders engaged in surprisingly complex contracts including forwards and options. Interestingly, none of the agreements were enforceable in official courts of law. Yet people engaged in them nonetheless.

Brokers experimented with ways to notify each other about defaulters, fines, subscription fees and membership requirements. The ultimate penalty was exclusion from Jonathan’s Coffee House.

As Adam Smith put it:

“They who do not keep their credit will be turned out, and in the language of Change Alley be called lame duck” (Smith 1766, 1982, p. 538)

Jonathan’s Coffee House eventually became the London Stock Exchange. It's motto has survived until the present day: “My word is my bond”.

Some of our most respectable financial institutions were born in coffee houses such as insurance firm Lloyd’s of London (formerly, Lloyd’s Coffeehouse, where merchants met to contract maritime insurance), the Philadelphia Stock Exchange (formerly, Merchants Coffee House) and auction house Sotheby’s.

It took more than a century for the English government to recognize that the broker’s private arrangements born in Jonathan's Coffee House “had been salutary to the interests of the public” and that the rules were “capable of affording relief and exercising restraint far more prompt and often satisfactory than any within the read of the courts of law” (London Stock Exchange Commission, 1878, p. 5).

What Decentralized Finance Can Learn from the Early Days of Capital Markets

The previous section summarizes how Professor Edward Stringham describes the early days of the London Stock Exchange in his book “Private Governance: Creating Order in Social and Economic Life”.

The rise of the London Stock Exchange illustrates an instance where the market itself created efficient rules for securing property rights, absent government regulation. Stringham argues that private governance can fulfill a key role in creating and enforcing rules when regulators and courts lack the knowledge or a way to do it in a cost-effective way.

The emerging decentralized finance ecosystem (DeFi) seems to share many features with the rise of corporations and stock exchanges in the 17th and 18th centuries.

Back then, the joint stock company was a phenomenal financial innovation, a new way to pool and coordinate human work for the fulfillment of projects that were unaffordable by individual investors. It enabled entrepreneurs to raise funds from the public and small investors to profit from the gains of such ventures.

DeFi is a new chapter in this long story towards financial inclusion. Cryptoassets can be transferred across boundaries at near zero cost enabling entrepreneurs to crowdfund projects where very small investors can participate (and profit!) from tokenized ownership.

With just an Internet connection, anyone can participate in the new world of finance.

As the DeFi ecosystem grows, a number of situations will require resolution:

- What cryptoassets should be accepted in decentralized exchanges such as Uniswap?

- What cryptoassets should be accepted as collateral in algorithmic stablecoins such as MakerDAO or yield generating applications such as Compound?

- What to do in case a hack compromises a smart contract?

The history of the London Stock Exchange can help us envision how regulation will evolve in DeFi.

In the early days, buying and selling crypto in Bitcoin forums was the equivalent of buying and selling stock on Change street. Mt.Gox was the first (unfortunate) equivalent to “coffee house regulation” in DeFi.

Just as in the early days of the stock exchange, this new financial ecosystem needs a regulatory body against "lame ducks" and to prevent that these new tools are used for illicit activities.

As in the early days of modern financial systems, governments lack the capacities to regulate a DeFi industry that is natively digital and global. But purely private and centralized regulation, which so far has been provided by centralized exchanges, lacks community involvement and tends to create monopolies.

In order to prosper, the decentralized finance ecosystem needs a more formal and sophisticated type of regulation mechanism. A mechanism that is trustworthy, impartial and that shares the decentralized nature of crypto markets.

The DeFi ecosystem needs a decentralized mechanism for self-regulation.

Kleros' Token Curated Registry: Private Compliance for the DeFi Ecosystem

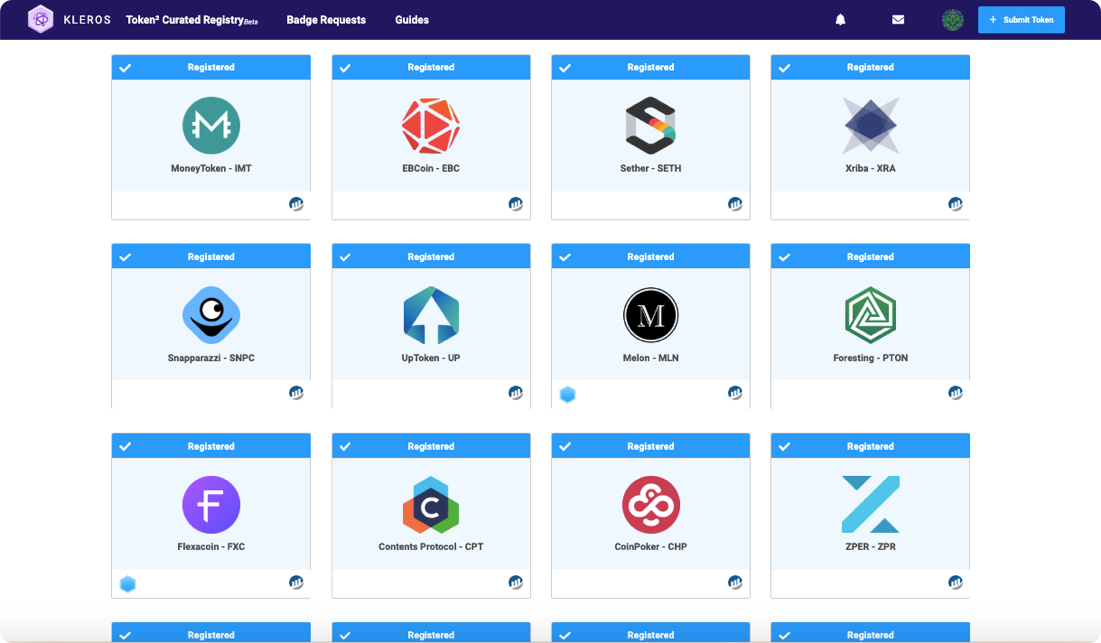

In March 2019, Kleros launched the Token Curated Registry of Tokens (T2CR). This was a list to which anyone could submit tokens and other users could vet them following a number of predefined rules.

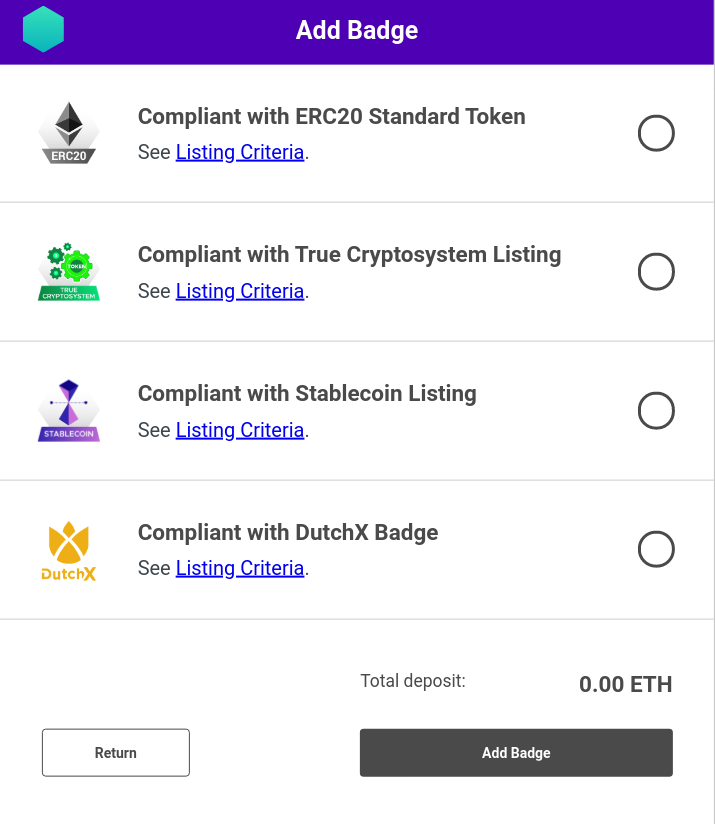

In order to have a token accepted into the list, it had to comply with some minimal conditions such as not having a malicious address. Then tokens could apply for badges having some desirable qualities such as being ERC 20, being a stablecoin, etc.

Based on these badges, different agents could make decisions to accept the tokens into different places. For example, being listed into exchange Ethfinex, DutchX or Uniswap.Ninja.

In the future, other badges could be created by defining what are the compliance conditions: for example, with what conditions should comply a token to qualify as an acceptable collateral in Compound?

After defining the rules for a "Compound Badge", projects would make submissions and users would vet them so only those compliant would be accepted.

In this way, Kleros T2CR was the first embryonic attempt of the DeFi ecosystem to self-regulate in order to prevent that investors will fall prey to scammers and opportunistic agents.

Public/Private Governance and the Future of Decentralized Finance

The regulation of financial markets has gone a long way since the early days of the gentlemen's clubs in London coffee houses. After starting as a purely private governance endeavor, the regulatory body for today's global financial infrastructure is a multi-stakeholder mechanism which encompasses public and private actors.

The DeFi ecosystem is likely to go a similar route towards collaboration between public and private institutions for keeping the system safe and protecting investors.

As the markets mature and larger amounts are transacted in DeFi, public bodies may delegate some compliance verification tasks to specialized private governance actors such as Kleros (among others) while keeping a supervisory role over the system as a whole.

A more widespread adoption of the Kleros Token Curated Registry can be an excellent first step for the regulation of the emerging DeFi ecosystem. A method that is native to the internet age and more sophisticated than the “coffee shop regulation” which is currently provided by centralized private actors.

It took more than a century for the English government to recognize that the broker’s private arrangements born in Jonathan's Coffee House “had been salutary to the interests of the public”. We can hope that, this time, it will be a private and public endeavor since the early days.

Where Can I Find Out More?

Join the community chat on Telegram.

Visit our website.

Follow us on Twitter.

Join our Slack for developer conversations.

Contribute on Github.

Download our Book